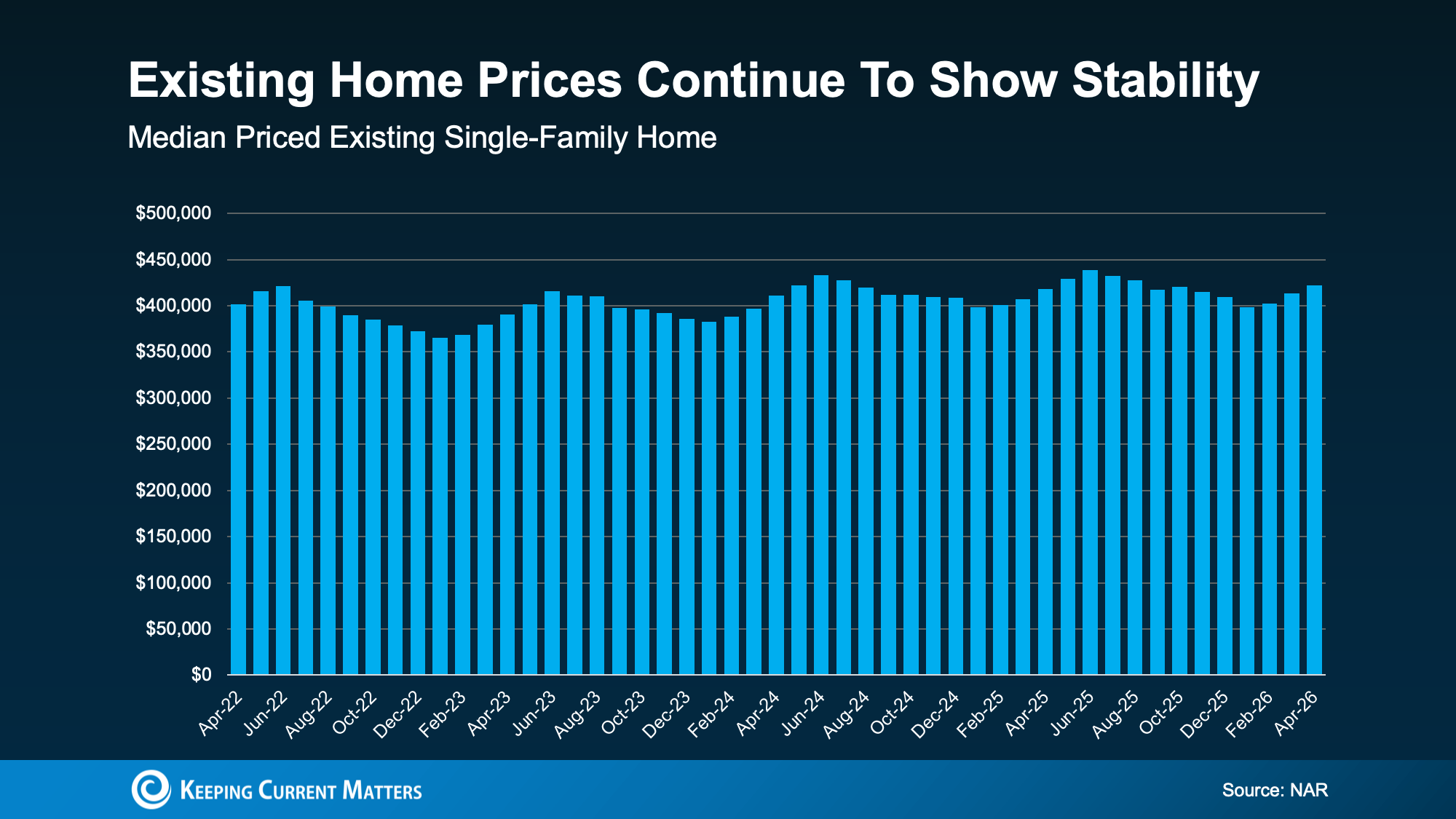

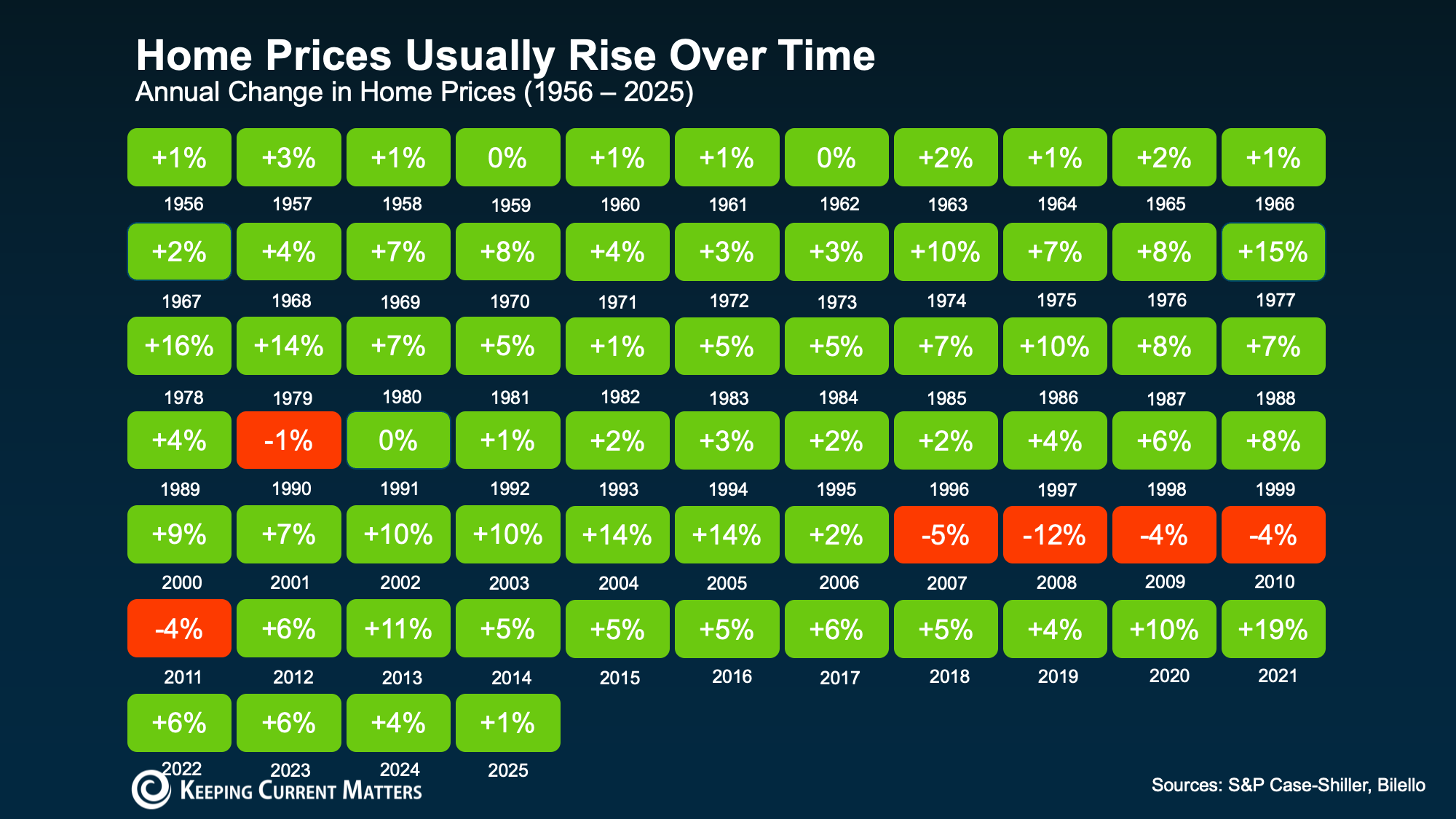

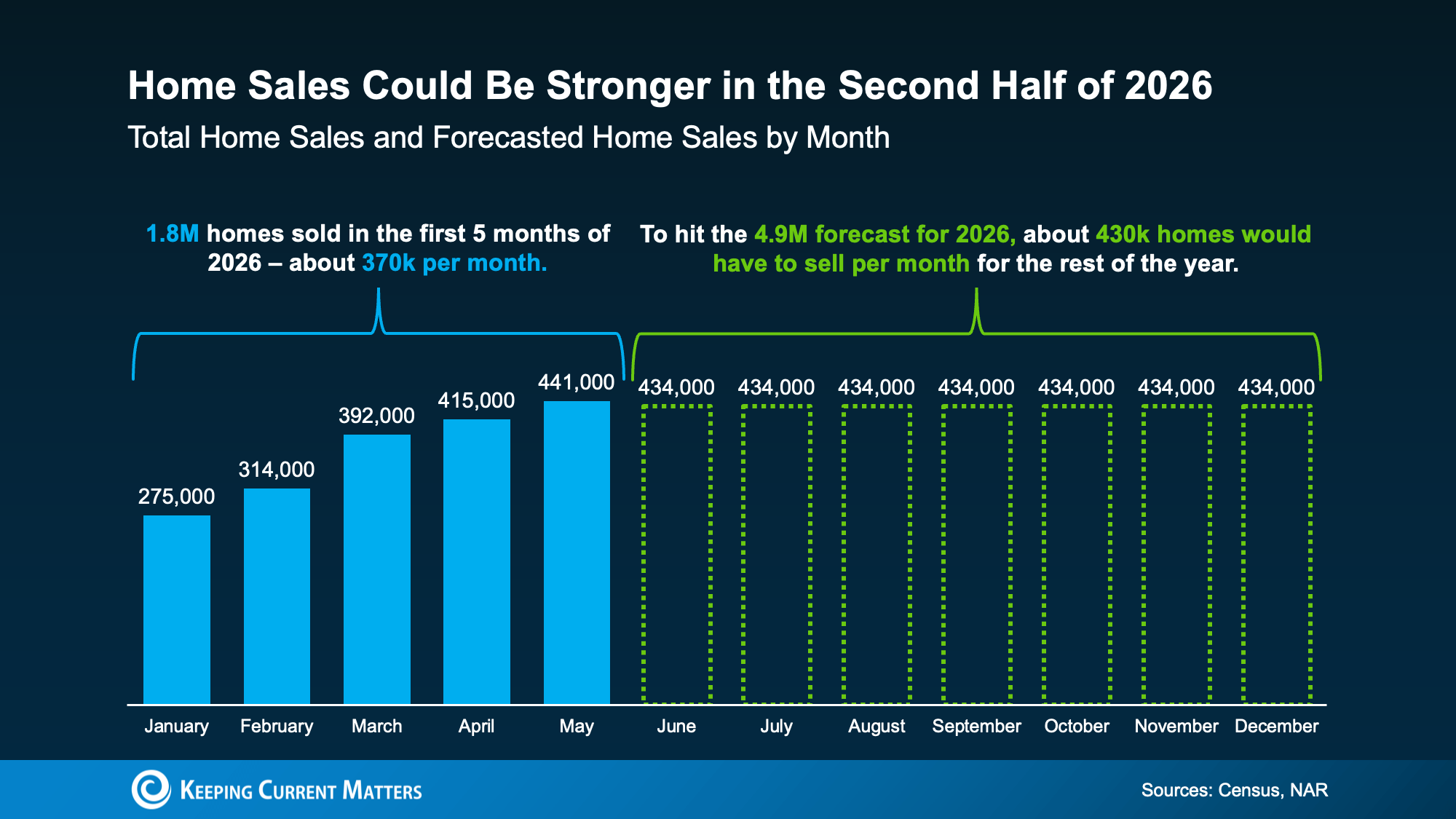

You’ve probably heard that home prices are cooling off. And that’s true – nationally. But zoom in on individual markets across the country, and the picture looks completely different depending on where you are.

Some areas are still seeing solid price growth. Others have gone flat. A few have actually dipped slightly negative. So, what’s causing all of that variation?

It All Comes Down to Inventory

Here’s the simple version:

-

When there are more homes for sale, buyers have options.

-

More options, means less competition.

-

Less competition means sellers can’t push prices as high.

On the flip side, when inventory is tight, buyers are competing over a small pool of homes, and that pushes prices up.

That dynamic is playing out right now in a really visible way across the country.

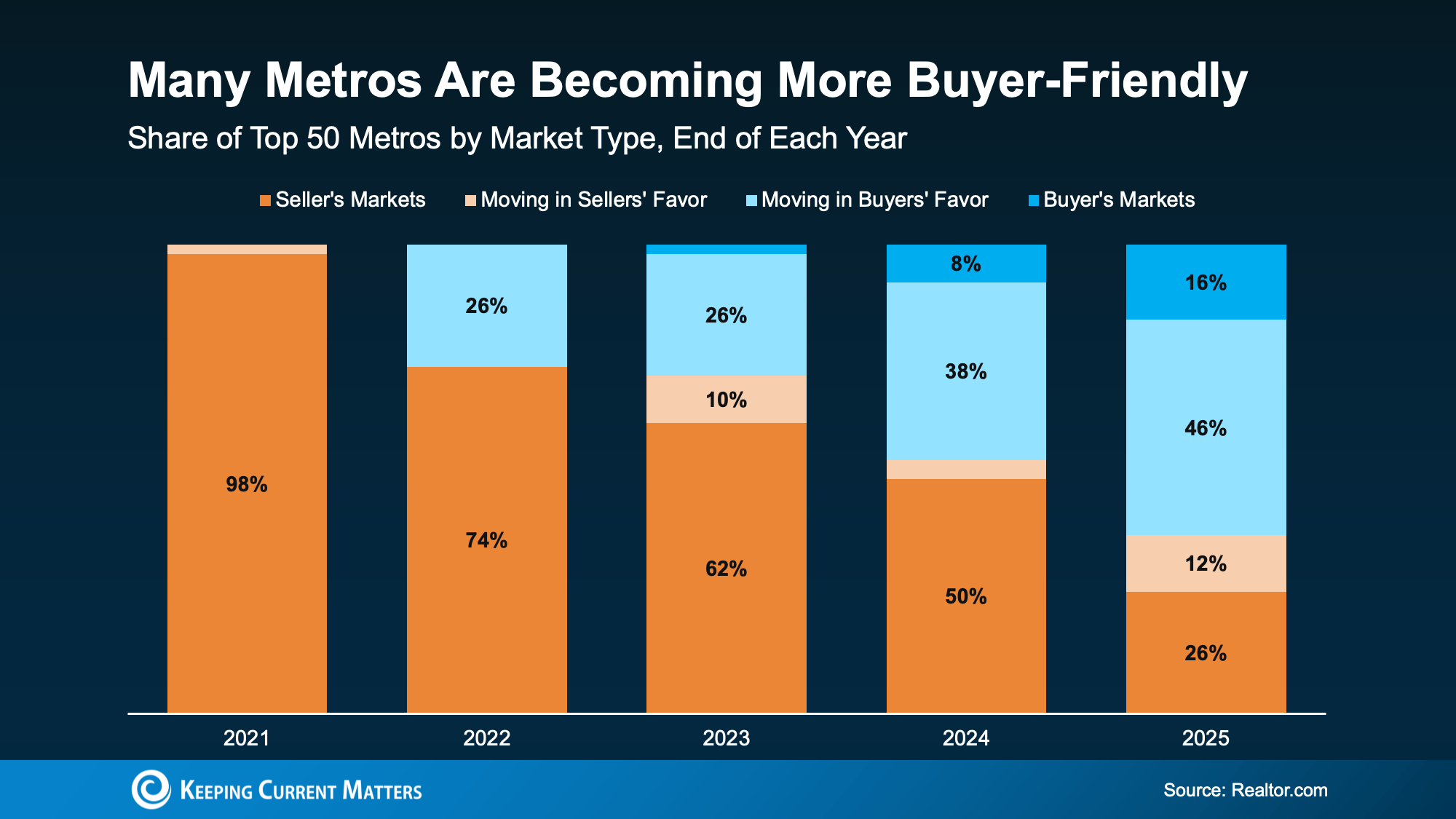

Markets where inventory has climbed back to, or above, normal pre-pandemic levels are seeing prices flatten or fall slightly. Markets where inventory is still well below those 2019 benchmarks are still seeing prices rise. As Lance Lambert, CEO of ResiClub, puts it:

“Home prices are still climbing a little year-over-year in many regions where active inventory remains well below pre-pandemic 2019 levels, such as pockets of the Northeast and Midwest.

In contrast, some pockets in states like Texas, Florida, and Colorado — where active inventory exceeds pre-pandemic 2019 levels by a solid clip — are seeing modest home price pullbacks or flat pricing.”

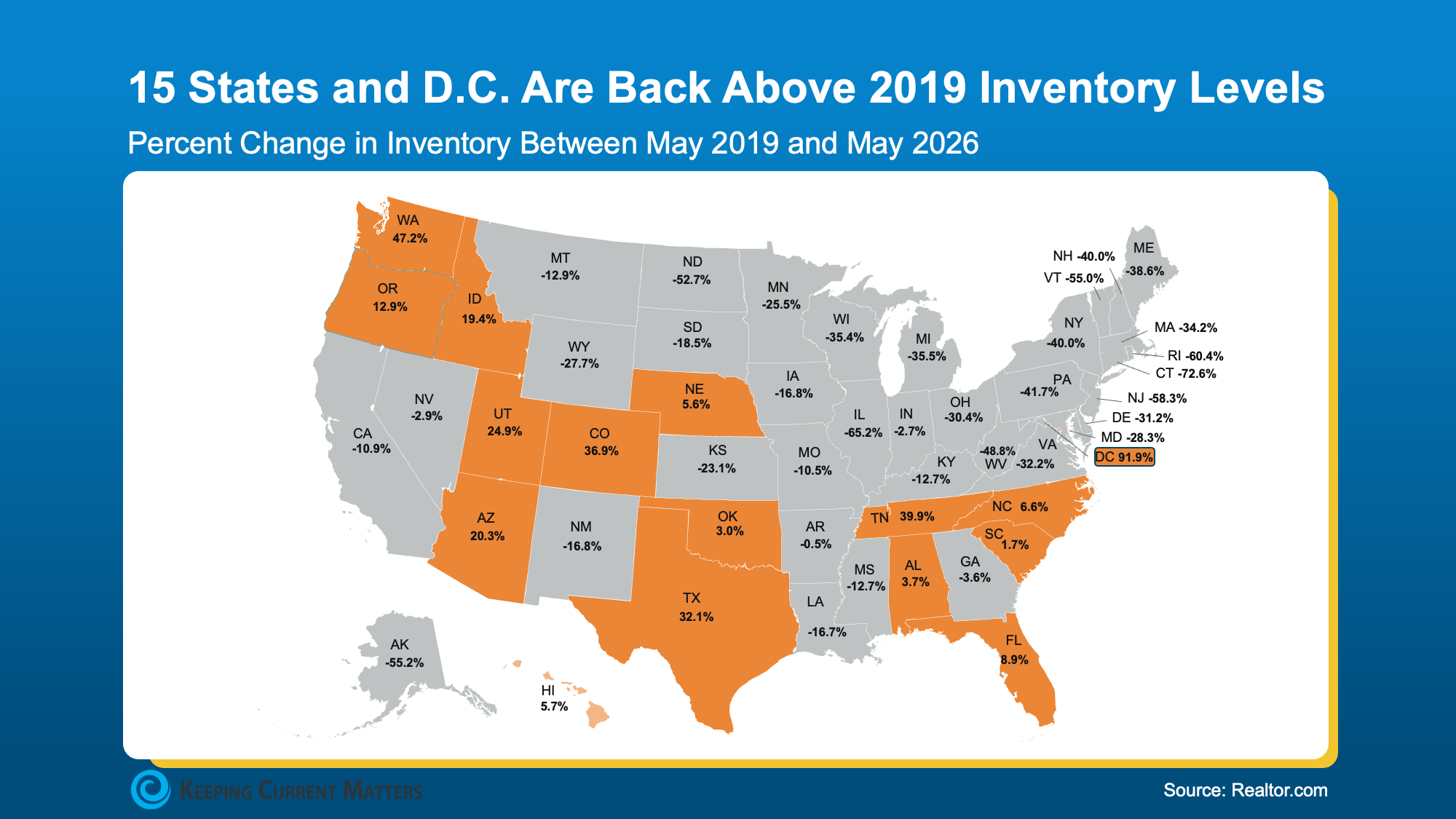

The Maps Say It All

Take a look at where inventory stands today compared to 2019. In most places (the states in gray below), inventory still falls short of where we were back then. And that’s exactly why prices are climbing, albeit moderately, in the vast majority of states.

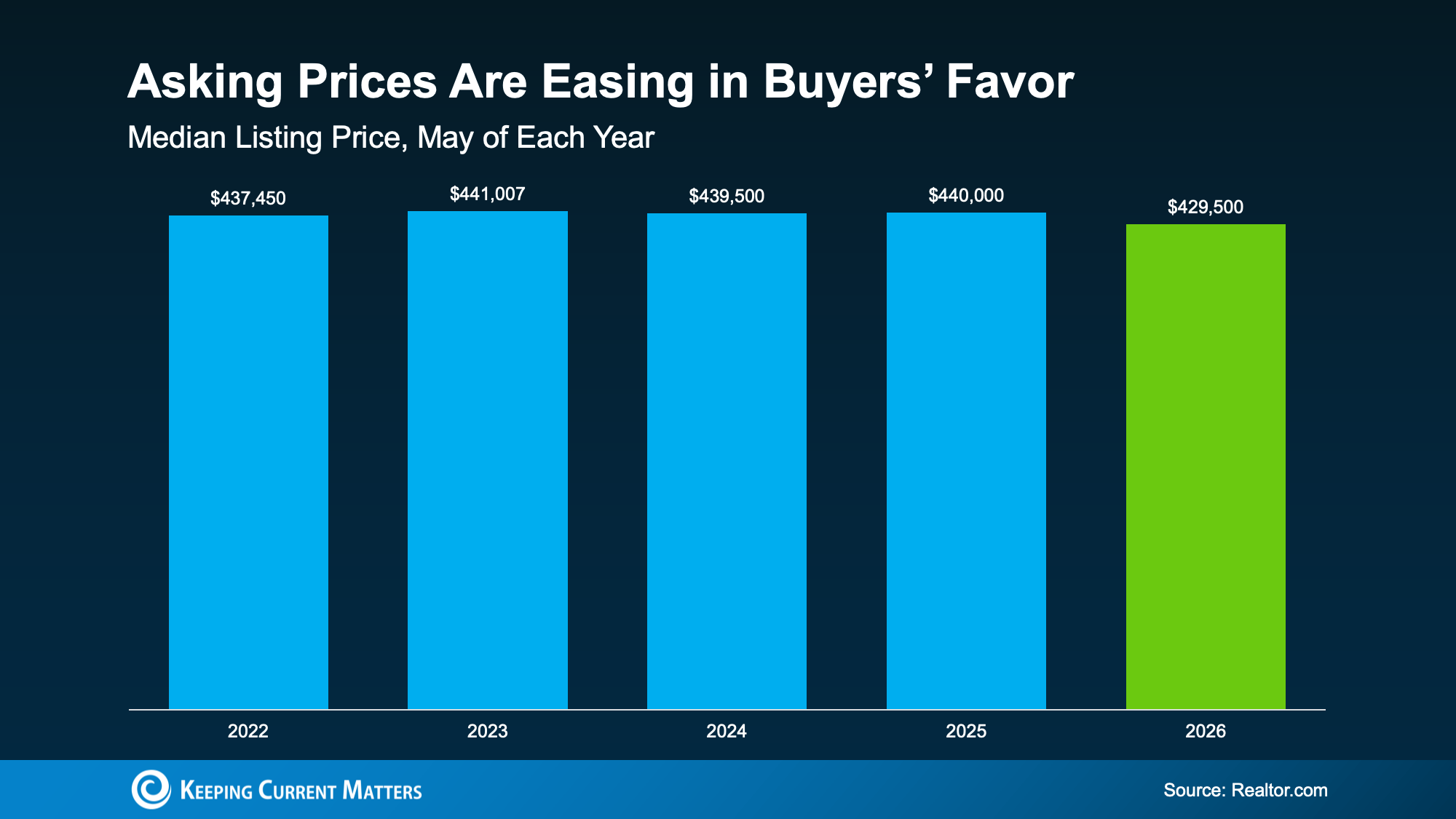

But you’re probably more interested in where prices are falling a bit, since that’s what is making headlines. So, let’s prove out how much inventory affects prices in those spots.

According to Realtor.com, 15 states and Washington, D.C. are now back above pre-pandemic inventory levels, and some by a wide margin (see the orange in the map below):

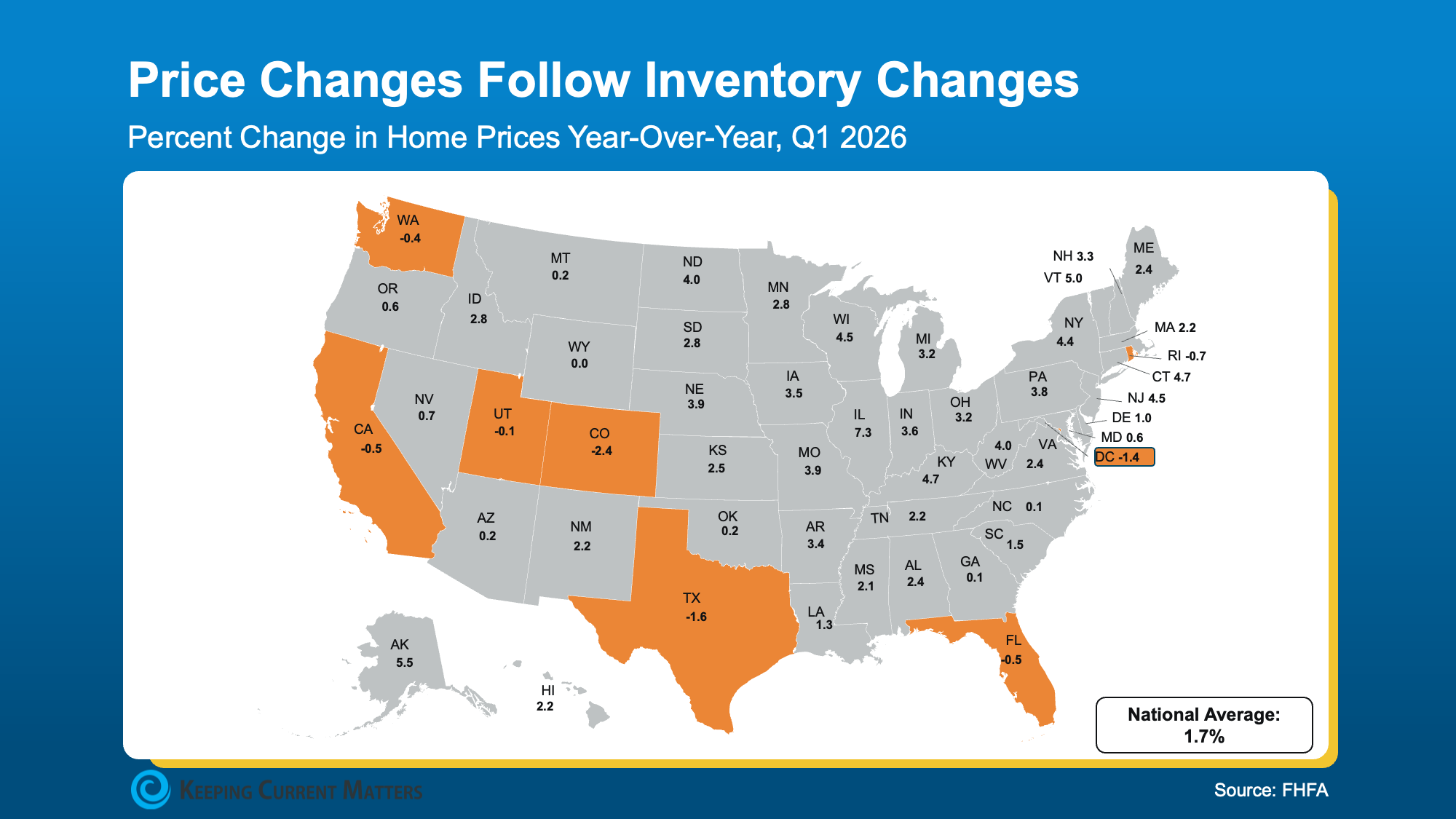

Now, let’s look at the latest Federal Housing Finance Agency (FHFA) data to see what’s happened to home prices in those same states over the past year (again, you’ll want to focus on the orange in the next map).

Now, let’s look at the latest Federal Housing Finance Agency (FHFA) data to see what’s happened to home prices in those same states over the past year (again, you’ll want to focus on the orange in the next map).

See how those line up pretty closely with the areas seeing more homes for sale today?

The overlap isn’t a coincidence. It’s cause and effect.

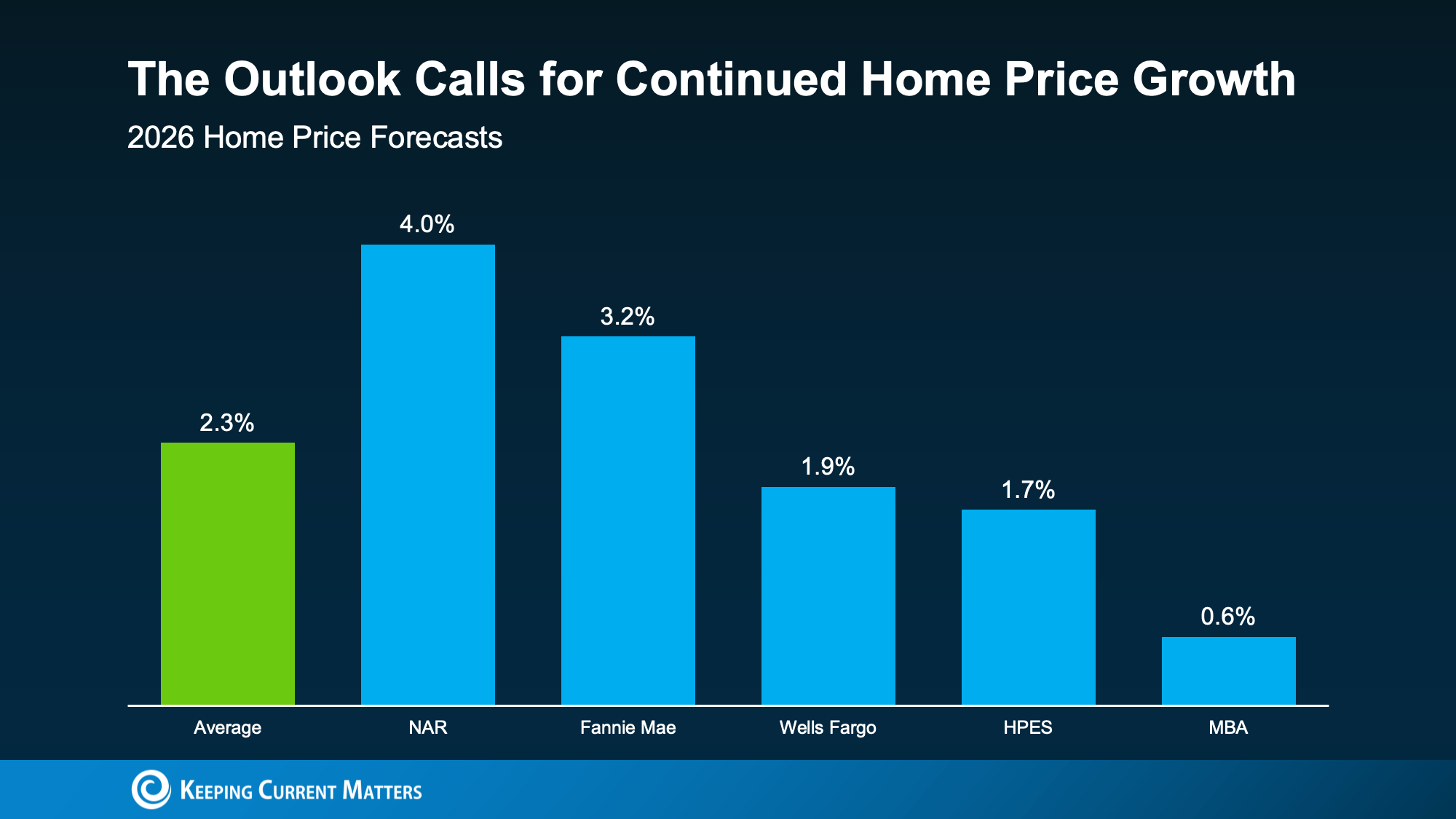

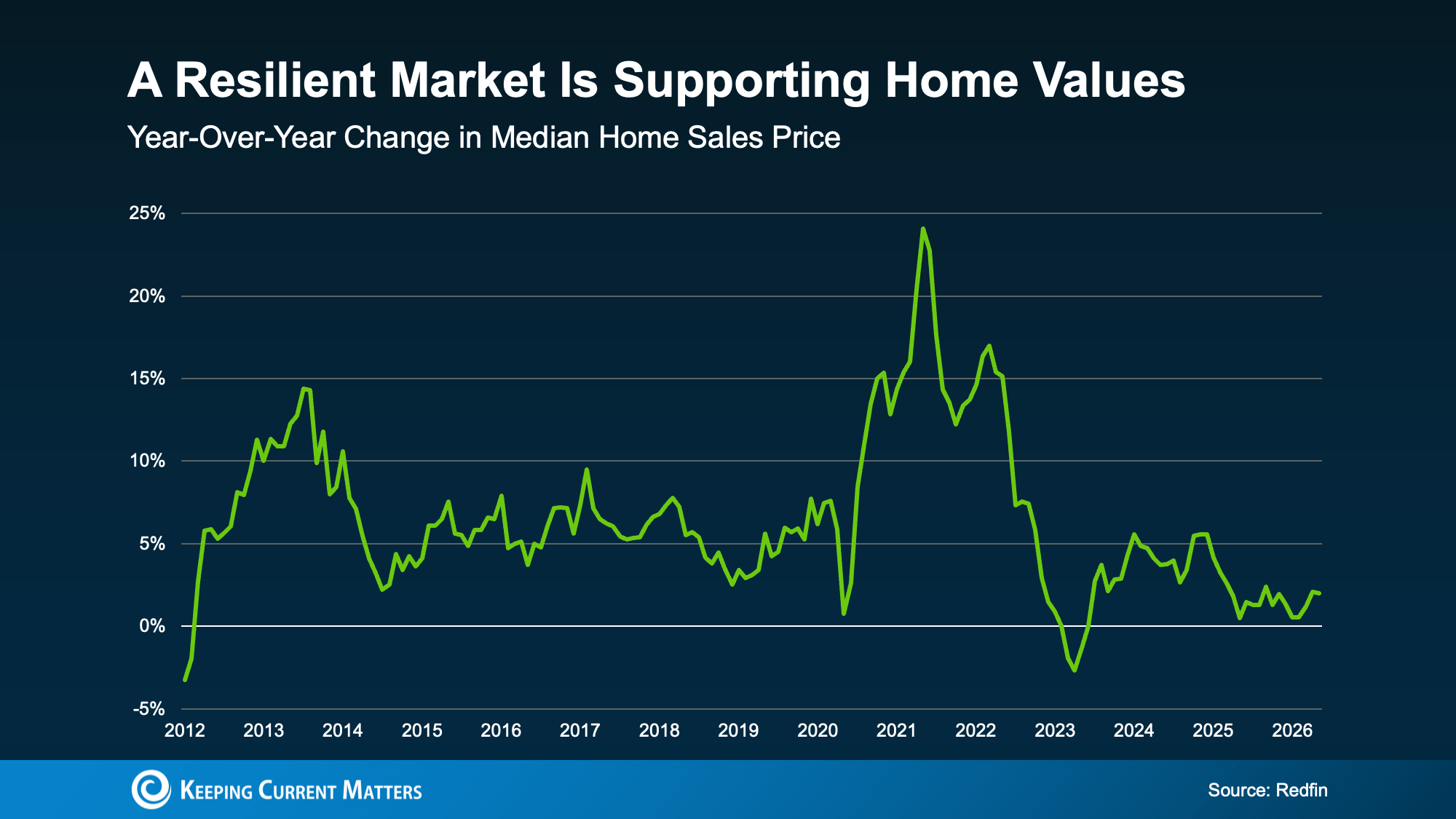

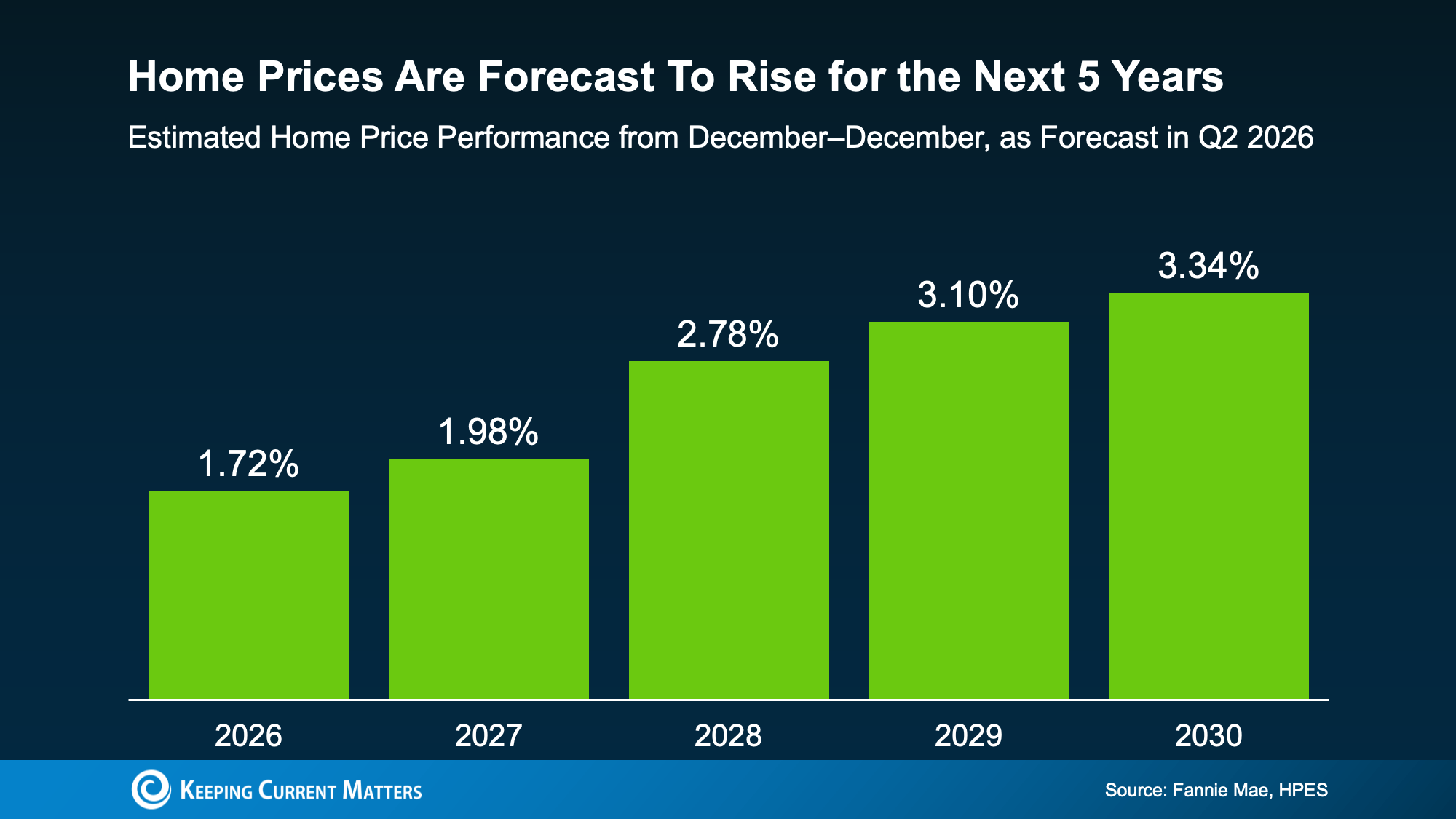

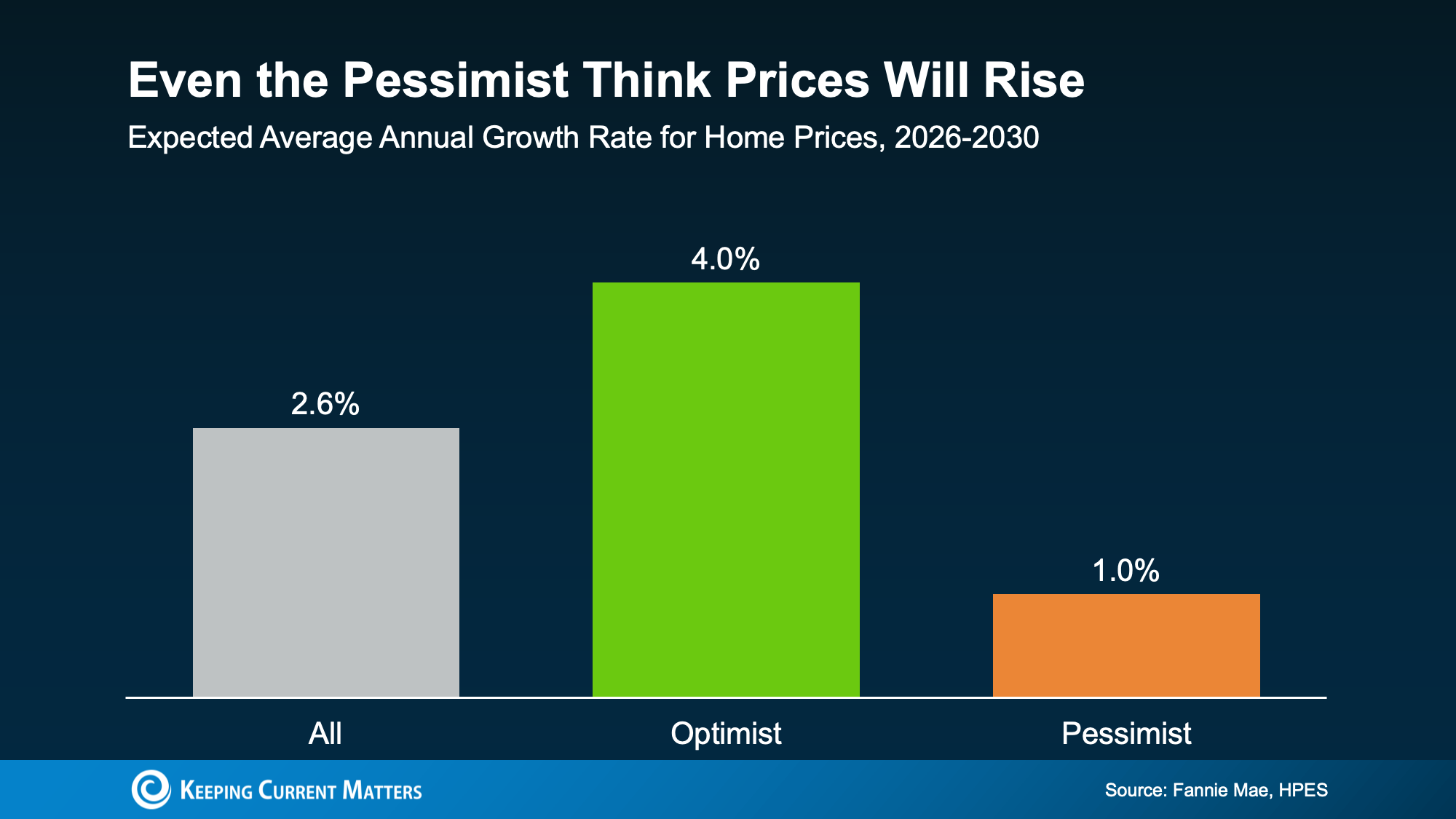

The national average of 1.7% price growth is accurate, but it’s an average of two very different stories happening at the same time – the few areas experiencing mild declines and the overwhelming majority that are still seeing prices rise.

What This Means If You’re Buying or Selling

If you’re a buyer, the market you’re shopping in matters a lot right now. In places like Texas, Colorado, or Florida, you may have real negotiating power – more choices, less competition, and sellers who are more motivated to make a deal. In tighter markets like much of the Northeast, you’re still likely facing a lot of competition.

If you’re a seller, pricing strategy is everything. In markets where inventory has risen, overpricing is one of the fastest ways to linger on the market and eventually sell for less than you would have with the right price from day one. In markets where inventory is still low, you’re in a strong spot, but getting your price right still matters if you want to attract serious buyers quickly. Either way, that’s where a local real estate agent earns their keep.

Bottom Line

When it comes to prices, where you are matters more than ever right now, and a local real estate agent is the best person to help you make sense of it.

Reach out to a local real estate agent today and work together to build a plan that fits your market.

KCM - July 2026

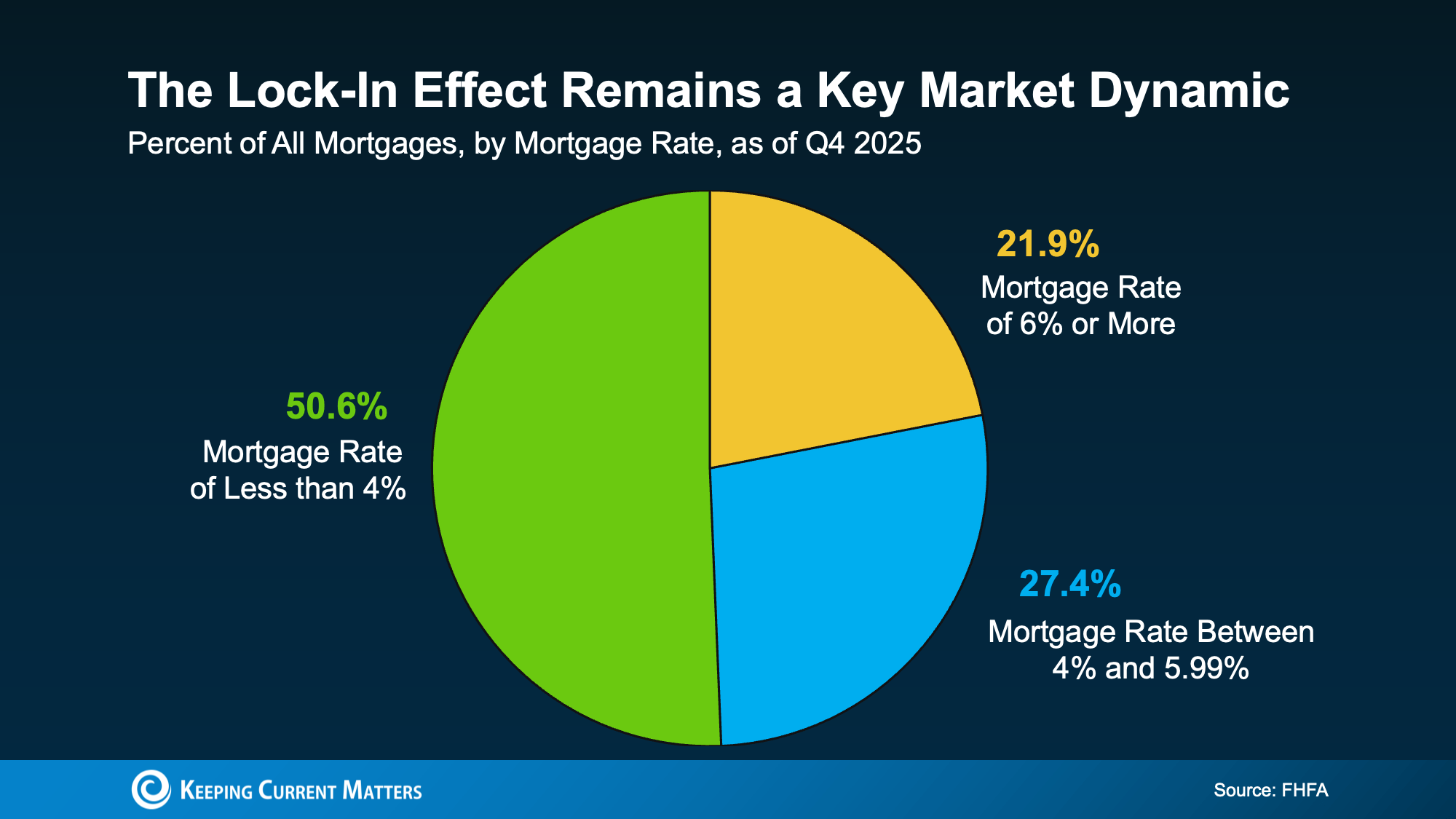

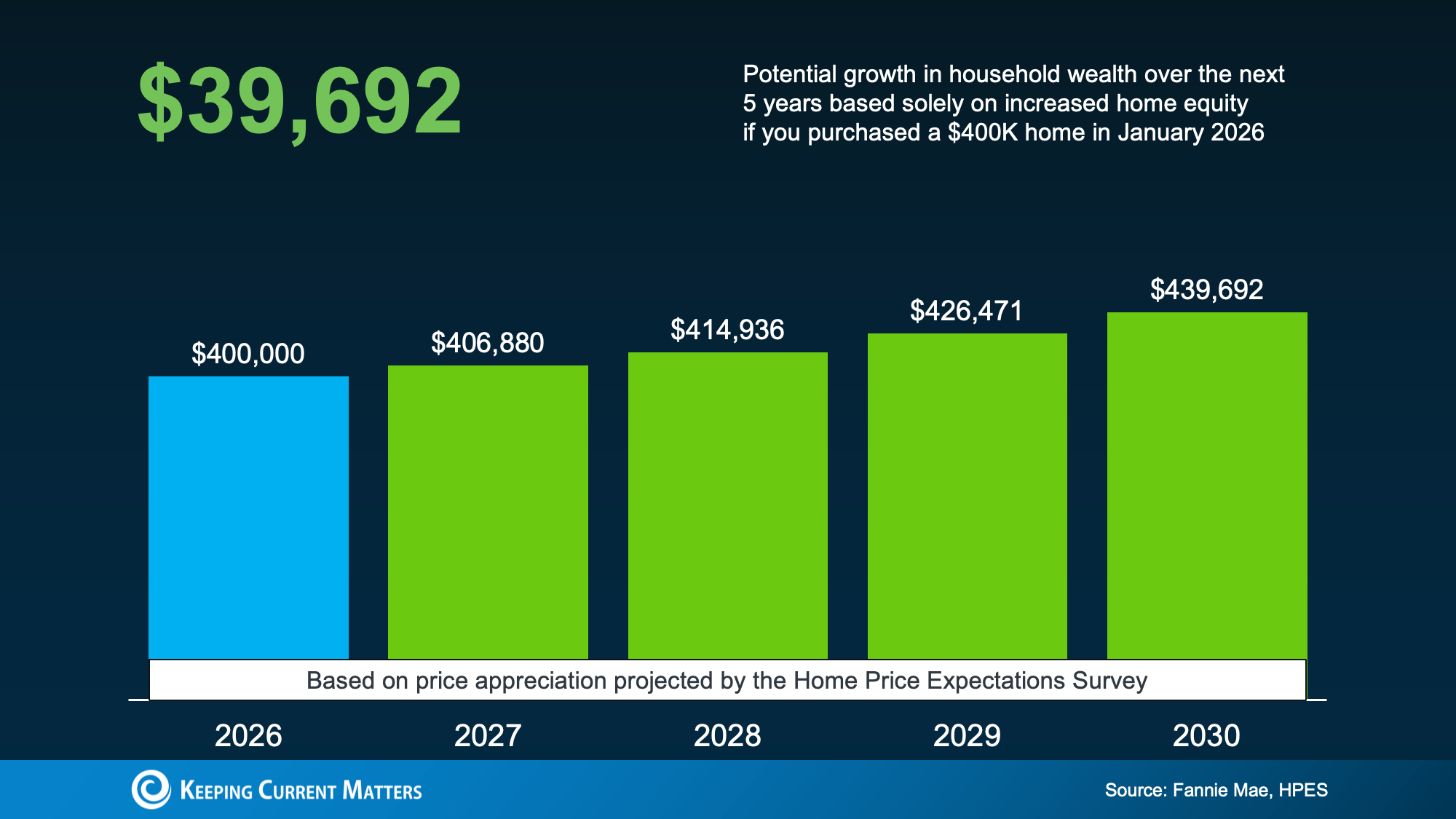

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time.

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time. That’s a big reason inventory stays tight. Those homeowners aren’t in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling.

That’s a big reason inventory stays tight. Those homeowners aren’t in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling. That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

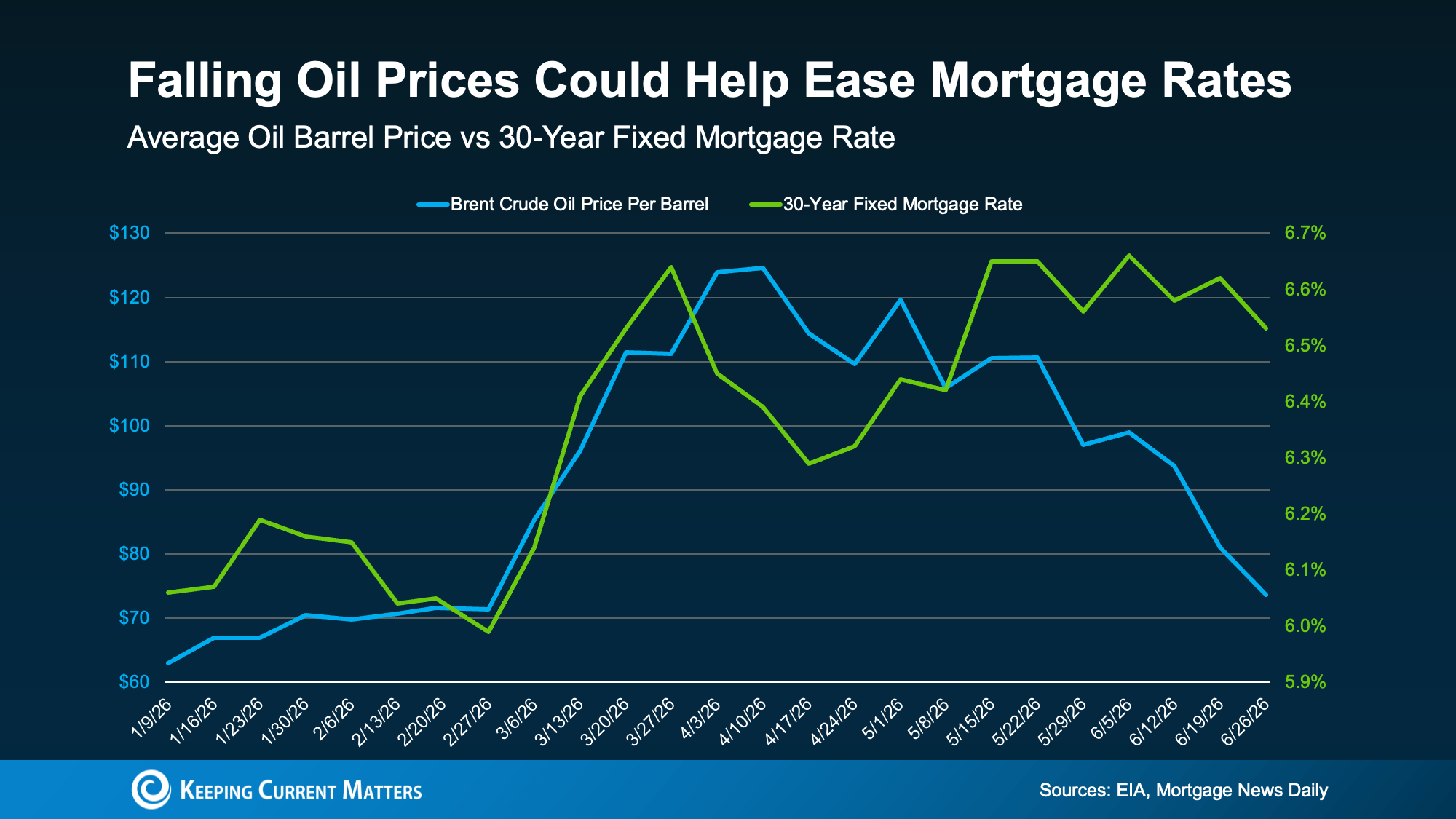

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it’s probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it’s probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?